The first pillar of the Government’s Housing Policy is Affordability. This includes:

Subsidies

The Ministry of Housing is mandated to provide housing units of different designs and costs to suit the needs of low to middle income families. The Ministry, through its agencies, is able to reduce costs by offering subsidised mortgage programmes and other concessionary financing for construction of the housing developments, thereby making it more affordable to purchase. The pricing of units are only decided by Cabinet when the development has almost been completed and full construction costs are known. The Government continues to encourage competitive pricing to keep overall costs down in keeping with its policy to provide affordable housing for the low and middle income earners.

The Cabinet, in 2006, approved the Housing Pricing Formula as follows:

- The Government absorbs all infrastructure costs, the land to be at a cost to be determined by the State; and

- A charge of no more than $5.00 per square foot be paid as a premium on the land.

This pricing formula equates to a subsidy of, on average, approximately 40 percent to be applied to the housing units.

Rental Programme

Rent To Own:

The Rent to Own (RTO) programme was designed to facilitate those persons who, given their current financial situation, are unable to qualify for mortgage financing. This programme is based on the premise that once a person’s financial qualification is within one hundred thousand dollars ($100,000.00) of the cost of the allocated unit and he/she is less than thirty five (35) years of age, he/she will be eligible for the RTO programme. Subsequently, the client would then pay a Rent to Own fee for a period ranging from three to five years; of which two thirds is applied as a deposit toward the cost of the unit at the end of the period and the remaining one third is retained by the Corporation as an administrative fee.

The RTO programme thereby allows for the difference to be paid within the stipulated period after which the client would be re-assessed. If the client is still unable to qualify at the end of the five year period, the Rent to Own agreement could be extended for a further three years at the discretion of the Corporation. Persons, who are unable to qualify at the end of the extended period, would then be converted to a rental arrangement and their payments applied as such. If the person is able to qualify at the end of the RTO period, he/she will be processed for a mortgage by the TTMB or another financial lending agency.

Rentals:

Post 1982, the National Housing Authority (NHA) constructed apartments for rent and indexed the monthly rate to the income of beneficiaries on a variable sliding scale between a minimum and maximum rental rate of $100 – $350.

Fast forward to 2017, the Housing Development Corporation (HDC) continues to provide rental units under the Accelerated Housing Programme to fulfil the needs of citizens such as our senior citizens who are unable to qualify for a mortgage. Rental rates for the newer units are also indexed to the income of beneficiaries, on a variable sliding scale.

Subsidised Mortgages (TTMB):

Accessing affordable mortgage options has been made even more possible with the Trinidad & Tobago Mortgage Bank (TTMB) restructured subsidized mortgage regime.

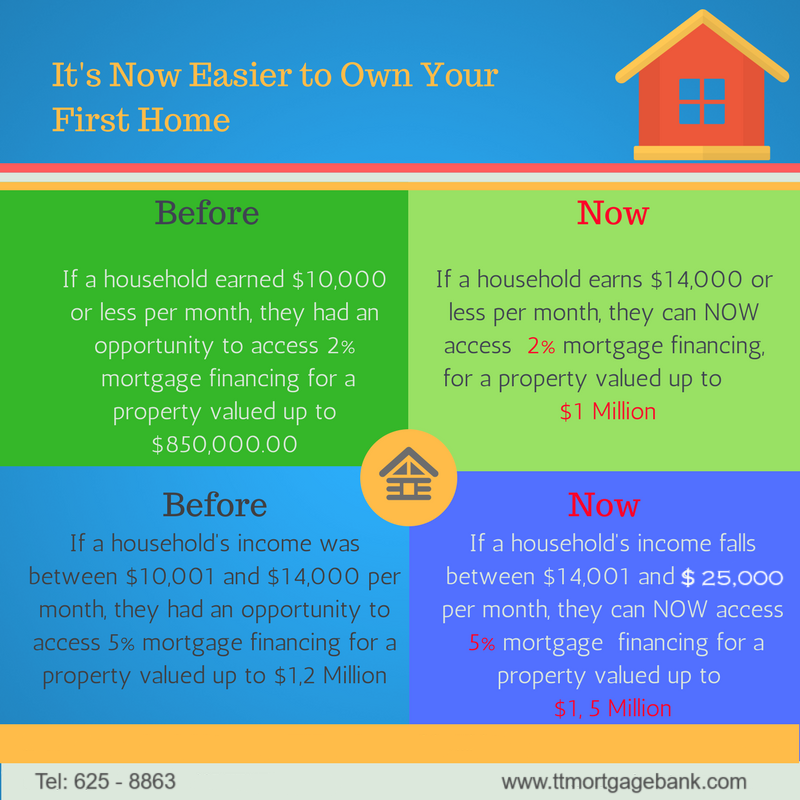

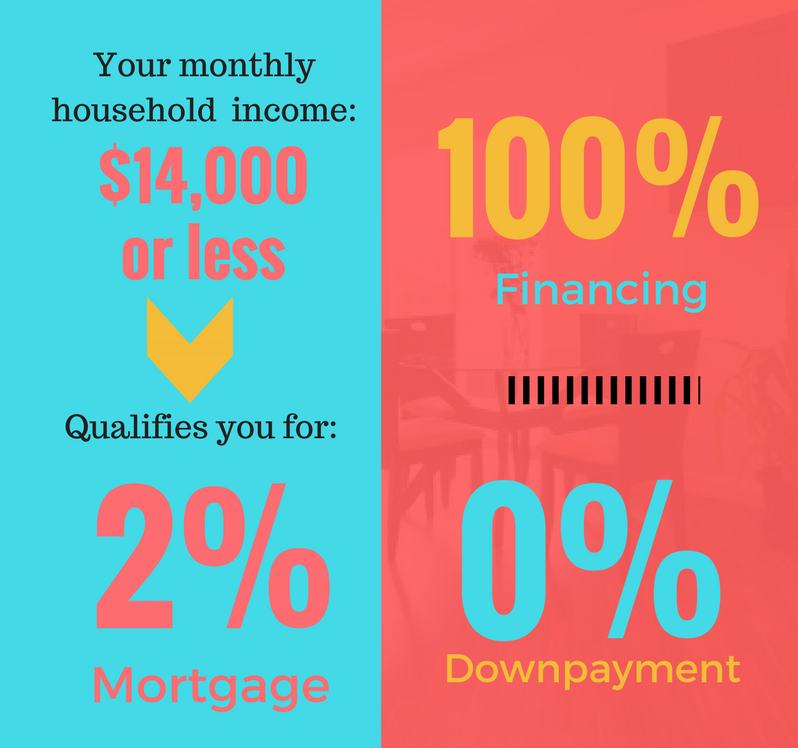

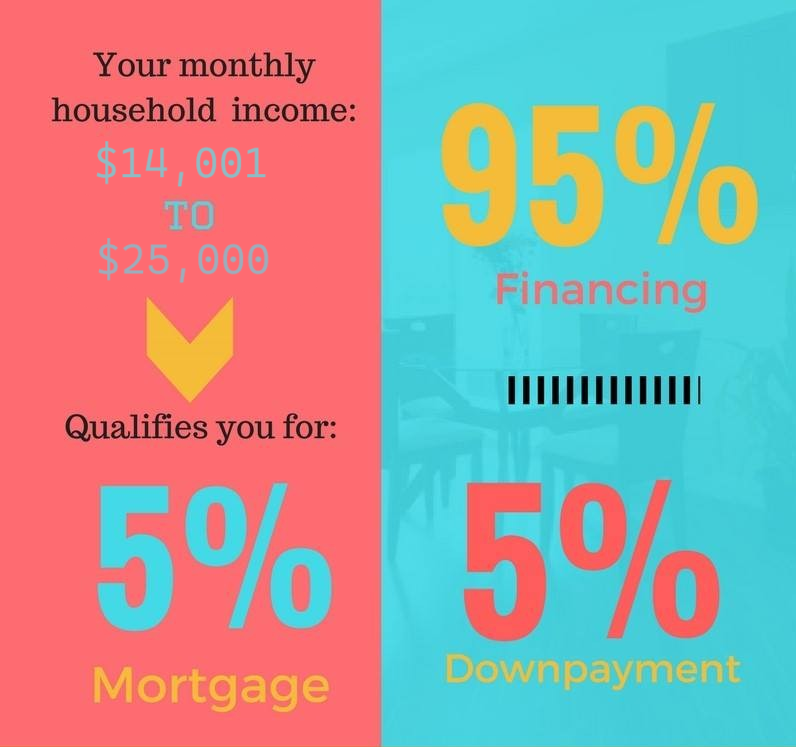

To cater to the needs of the lower and lower income earners, the affordable financing regime was expanded in early 2015 to include a 5% mortgage interest rate for first time home owners whose monthly earning was not in excess of $25,000.00. This would afford them the opportunity to purchase a property up to $1.2M and qualify for 95% financing on properties valued at $1.2M.

By September, 2016 the Government further modified the qualifying income and property value to reflect a more realistic picture of the marketplace and give citizens a greater ability to access affordable housing solutions.

In the 2017 Budget Statement, Finance Minister, the Honourable Colm Imbert articulated that:

‘to ensure that the housing needs of our lower and middle income groups are being met, the Government has taken the decision to increase the qualifying monthly income from $10,000 to $14,000 and the property value from $850,000 to $1M in order for persons to access the 2% financing regime; in respect of the 5% facility, the lower limit of $10,001.00 has been moved to $14,001.00 with a higher limit of no more than $25,000.00. This would allow for the purchase of properties up to $1.5M.’

These amendments are expected to benefit more than 6,000 families who are potential beneficiaries of the State’s housing programme. Other persons seeking to purchase on the open market can also benefit from this mortgage financing regime.